QUICK SUMMARY

This guide explains how fintech teams can design UCaaS that keeps voice, video, and chat secure and compliant, without losing context or control as communication volumes grow.

Fintech communication systems don’t break when traffic is low.

They break during peak transactions, when calls spike, chats pile up, and CRM sync delays turn into compliance blind spots.

Financial communications carry more weight than retail or SaaS support. Every call, message, or video interaction can become part of an audit trail. That’s why UCaaS for fintech can’t be treated as a generic communication layer. It has to behave like a controlled, traceable system, even under load.

And here the challenge isn’t adding voice, video, or chat. It’s designing them to work together securely, stay compliant, and sync with CRM in real time without creating gaps. And this is where an AI-driven approach of Ecosmob helps, not by replacing controls, but by monitoring conversations, detecting anomalies, and keeping context intact as interactions scale.

This guide breaks down how UCaaS for fintech should be designed when security, compliance, and real-time visibility are non-negotiable. Let’s see.

What are the Risks of Using Generic UCaaS Platforms for Regulated Financial Communications?

On the surface, generic Unified communication platforms seem like an easy choice. They bundle voice, video, and chat and promise quick deployment. But in regulated financial environments, those conveniences often hide risks that only show up later, during audits, traffic spikes, or incident reviews. This section looks at where generic UCaaS platforms fall short when compliance and control really matter.

Limited control over call flows and data storage

Generic UCaaS platforms usually come with predefined call flows, logging rules, and storage options. That works fine for general support teams, but fintech communication needs tighter control. Some calls need to be recorded, others masked, and data often must stay within specific regions. A secure UCaaS for financial services needs these decisions built into the system, not handled through manual overrides.

Compliance features that don’t fully fit fintech needs

Most platforms advertise compliance features, but they’re designed to work broadly, not deeply. Recording and retention settings exist, yet how they’re enforced is often hidden from the teams using them. When regulators ask how policies are applied in real scenarios, fintech teams are left relying on vendor assurances instead of clear system behavior.

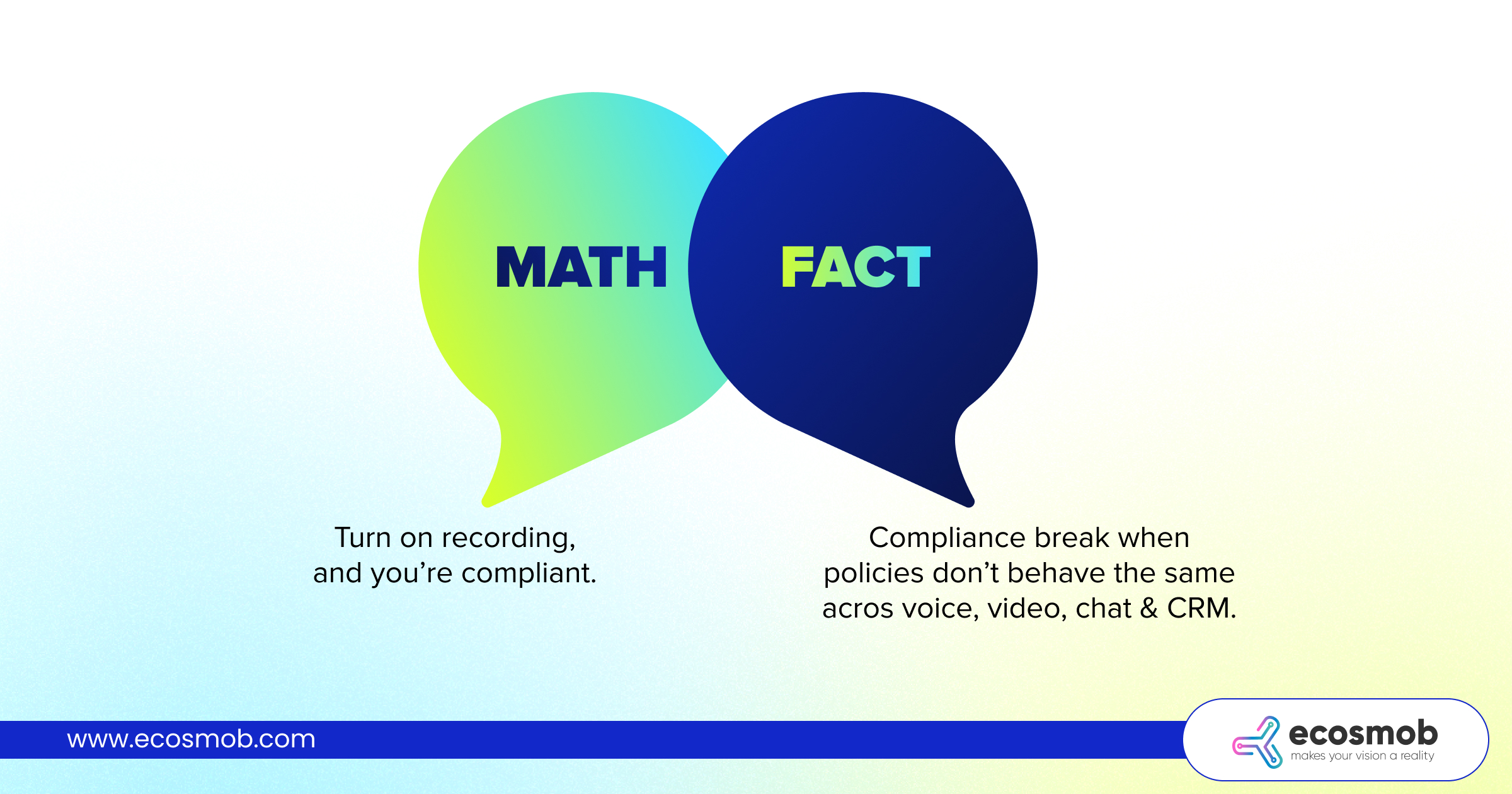

Recording and retention rules that are too rigid

Recording and retention rules that are too rigid

Generic UCaaS platforms tend to apply the same recording and retention rules across voice, video, and chat. In fintech, that rarely works. Retention can vary by transaction type, customer profile, or geography. A compliant UCaaS platform should adjust to those conditions automatically, instead of forcing teams to patch gaps later.

Heavy dependence on vendors during audits or incidents

When something goes wrong, fintech teams need quick access to logs, timestamps, and communication history. With generic UCaaS platforms, that access often depends on vendor tools and response times. This loss of direct control can slow investigations and increase risk at exactly the wrong moment.

Not sure how your current UCaaS will hold up during audits or traffic spikes? A short review can bring clarity.

Core Compliance Requirements That Shape Fintech UCaaS Design

Before choosing tools or features, fintech teams need clarity on what the communication system is actually responsible for. In regulated environments, voice, video, and chat aren’t just channels; they’re records. How those records are captured, stored, and accessed shapes the entire UCaaS design.

Compliance regulations (HIPAA, GDPR… influence everything from call routing to CRM sync timing. Recording policies, data residency, encryption, and access controls can’t sit on the side. They need to be part of the system’s core logic. When compliance is treated as an add-on, gaps are inevitable, especially as volume grows.

Common Compliance Gaps in Fintech Voice and Chat Systems

Most compliance issues don’t come from obvious failures. They come from small oversights that compound over time.

A common gap is partial coverage. Voice may be recorded correctly, but chat logs are incomplete or stored elsewhere. Video calls used for verification may not follow the same retention rules. This fragmentation makes audits harder than they should be.

Another issue is missing context. Conversations exist, but they’re not reliably tied to customer records, agents, or transactions. Without that linkage, proving intent or sequence during a review becomes difficult.

These gaps usually appear not because teams ignore compliance, but because the communication system wasn’t designed to handle it consistently across channels.

When security, compliance, and scale matter, it helps to review your UCaaS design with specialists in regulated fintech systems.

Designing Secure Voice Architecture for Fintech UCaaS

Voice remains the most sensitive channel in fintech. It’s where identity is verified, transactions are discussed, and decisions are confirmed.

A secure UCaaS for financial services needs strong call control from the start. That includes authenticated signaling, protected media paths, and clear rules around when calls are recorded or masked. Fraud prevention and monitoring should happen in real time, not after issues surface.

Just as important is visibility. Teams should be able to trace a call end to end, who handled it, what policy applied, and where the record lives, without relying on vendor support to answer basic questions.

HIPAA architects always ask:

“Who should not have access to this conversation?”

Fintech teams usually ask:

“Who needs access?”

That difference changes how UCaaS should be designed.

1. Secure Video Communication in Regulated Financial Workflows

Video is increasingly used for onboarding, advisory calls, and escalations. But many fintech teams underestimate how quickly it becomes a compliance surface.

Secure video design means more than encryption. It requires clear session ownership, identity validation, and consistent recording behavior when required. Some interactions must be recorded, others explicitly excluded, and that decision often depends on context.

When video sits outside the main UCaaS flow, it creates blind spots. Bringing it into the same control layer as voice and chat reduces risk and keeps policies consistent.

2. Designing Compliant Chat and Messaging for Fintech Teams

Chat feels lightweight, but in fintech it carries the same regulatory weight as voice.

Messages need to be captured completely, stored securely, and linked to customer records. That includes bot interactions, agent handoffs, and escalations. Gaps often appear when chat systems grow faster than the rules governing them.

A compliant UCaaS platform treats chat as a first-class channel. Retention, monitoring, and access policies should apply automatically, without relying on manual cleanup or external exports.

3. UCaaS Features That Directly Affect Fintech Customer Experience

Customers may not see compliance controls, but they feel their effects.

Poor UCaaS design shows up as repeated verification, dropped context between channels, slow escalations, or inconsistent responses. A well-designed system does the opposite. It keeps conversations smooth, preserves context, and reduces friction without cutting corners.

Real-time features of UC like unified agent views, intelligent routing, and real-time context sharing don’t just improve efficiency. They build trust, which matters more in fintech than almost anywhere else.

The Long-term Cost of Ignoring Compliance in Fintech Communications

The Long-term Cost of Ignoring Compliance in Fintech Communications

Ignoring compliance rarely causes immediate failure. The cost shows up later.

Teams end up rebuilding communication systems under pressure, usually after audits, incidents, or regulatory changes. Vendor limitations become roadblocks. Migration becomes expensive. And trust takes time to recover.

Designing UCaaS for fintech correctly from the start costs less than fixing it later, both financially and operationally.

A practical approach to building UCaaS for fintech

The strongest UCaaS designs share a few traits. Channels are unified under a single control layer. Compliance rules are enforced automatically. CRM sync happens in real time. And AI is used to monitor, not override, governance.

This approach gives fintech teams flexibility without losing control. It also makes the system easier to adapt as regulations and business models evolve.

If you’re assessing whether your UCaaS is truly secure and compliant for fintech use, a focused conversation can help clarify the gaps.

Final Takeaways

UCaaS for fintech isn’t about adding more communication tools. It’s about designing a system that stays secure, compliant, and reliable under real-world pressure, and we at Ecosmob do that.

Voice, video, chat, and CRM need to work as one. Compliance needs to be built in, not layered on. And scalability has to protect control, not weaken it.

When those pieces come together, communication stops being a risk surface and starts supporting growth instead of slowing it down.

FAQs

Why can’t fintech teams rely on standard UCaaS platforms for compliance?

Because most standard UCaaS platforms are designed for general business use, not regulated financial workflows. They often lack fine-grained control over recording rules, data residency, audit trails, and real-time context handling, which fintech compliance demands.

How does AI actually help in UCaaS for fintech without creating new risks?

AI works best when it supports governance, not replaces it. In UCaaS for fintech, AI helps by maintaining conversation context across channels, monitoring interactions for anomalies, and flagging potential compliance gaps early, without bypassing human or regulatory controls.

Is real-time CRM sync really necessary, or is near-real-time enough?

In regulated environments, delays matter. Even small lags can break interaction timelines, create inconsistent records, and raise audit questions. Real-time CRM sync ensures conversations, decisions, and actions are logged accurately as they happen.

Which communication channel creates the most compliance risk in fintech?

It’s rarely a single channel. Most risks appear during channel switches, like moving from chat to voice or voice to video, where recording rules or context often reset if the UCaaS isn’t designed as a unified system.

Can fintech teams add compliance later as they scale?

They can, but it’s expensive and risky. Retrofitting compliance usually means reworking call flows, rebuilding integrations, and migrating data under pressure. Designing UCaaS for fintech with compliance built in from day one is far more sustainable.